Pandemic Behavior:

Over the past few weeks, everyone has heard a number of different perspectives around the state of research during the pandemic, the validity of available research methods, and how to prioritize research moving forward.

We know shopper behavior is changing and research will be required to understand the impact of these changes. After all, about half of US shoppers (47%) are saying they are stocking up on essential items. Overwhelmingly, this is because stocking up makes them feel safer (78%). In times of uncertainty, shoppers want to feel that they have provided for themselves and their family.

The most common stock up products are food items and water (93%), toiletries (74%), cleaning supplies (58%), medicine and health care items (45%) and pet supplies (41%). But what will this stock-up behavior mean for these diverse categories in the medium-term?

This, of course, makes us (and everyone) ask what the ‘new normal’ will look like. In order to understand research needs, we will need to understand the unique situation of each category or group of products.

Key Questions To Ask When Setting Research Priorities:

We want to suggest a more helpful and realistic perspective of the critical research priorities. These will necessarily be different, depending on industry and category.

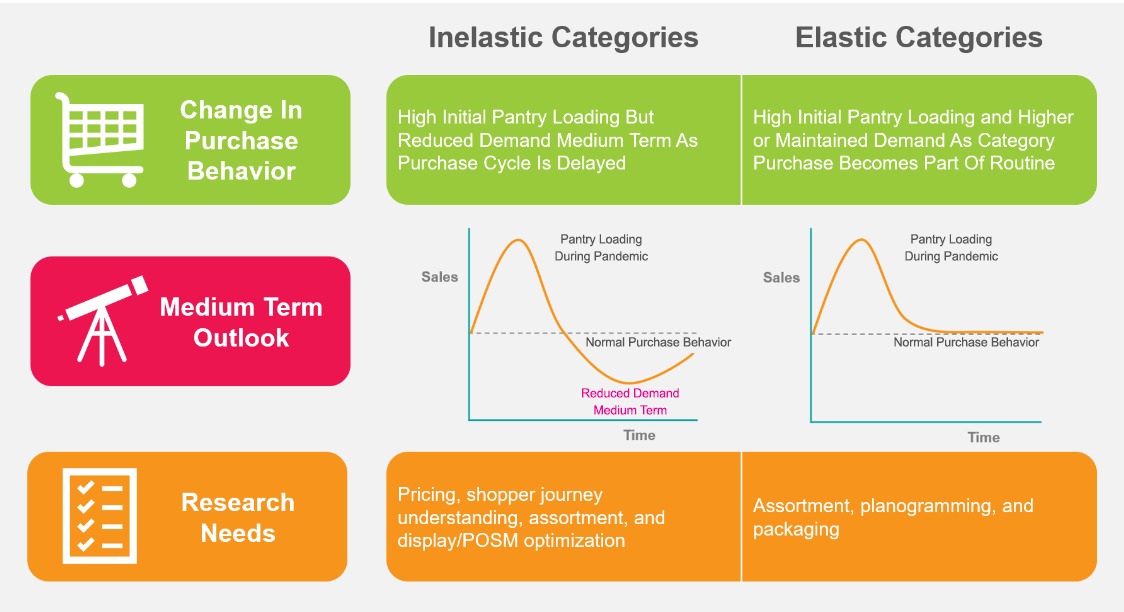

At a general level, the medium-term impact of the current situation on a particular group of products can be characterized based on 2 key questions:

- To what degree is the category being pantry-loaded?

- How elastic is the demand for the category?

The answers to these 2 questions will dictate the necessary research priorities in a post-pandemic world.

Inelastic Categories:

For categories with relatively inelastic demand that are currently being pantry loaded, a category contraction is likely in the medium-term. For example, baking categories like Yeast (up 601%), or staples like Dried Beans/Grains (up 297%) are seeing short term gains. But once the crisis has abated, will purchase remain at high levels? Will people still have the time to bake as much once they can leave their homes again? Will they still buy as many dry grains that have a long pantry life? Most likely they won’t.

Different category players are currently benefitting from product trial, even from shoppers who previously may have described themselves as ‘brand rejecters’. 85% of US shoppers feel brand doesn’t matter during stock-up at this time – instead they are grabbing whatever brand is available. Although this provides a short-term benefit for the brand, this relationship could end fast, as the purchase cycle for the category has been significantly delayed (due to inelastic demand).

So, for these inelastic categories, the situation is likely to become a share strategy in the medium term. And key category priorities will likely include pricing/sales, updated shopper journey understanding, secondary merchandisers (capturing shoppers before they get to the aisle), and assortment prioritization.

Elastic Categories:

Then there are other types of categories, such as those that are being pantry-loaded, but also have relatively elastic demand (e.g. having more chips on-hand may very well result in you eating more chips!). For these categories, a medium-term growth period is likely. These categories are currently experiencing unprecedented trial and re-engagement, with shoppers and consumers realizing they really enjoy these brands and products. They become part of the weekly shopping trip, which solidifies behavior and loyalty.

Shoppers will continue to buy brands in these categories that provide a good experience but that also handle the pandemic well. Brands that are seen as caring (both to customers and employees), empathetic, offer solutions instead of selling, while also offering information, will be the brands that leave a lasting impression in the minds of consumers after the pandemic.

Post-pandemic, these elastic categories are likely to be set up for continued growth, especially if they offer a compelling brand image and story. As a result, key category priorities will likely include assortment expansion, planogramming, package optimization, and even larger scale department or category ‘re-invention’ initiatives (for sustained growth).

How to Succeed Post-pandemic:

Depending on how different companies and categories align with these characteristics, success will be determined by a company’s ability to focus on the right research topics, unique to their needs.

For categories that tend to be more inelastic in their demand, now is the time to begin focusing on research efforts around post-pandemic pricing, shopper journey understanding, assortment, and display/POSM optimization.

For categories that tend to be more elastic in their demand, areas of research focus should include assortment, planogramming, and packaging.

Of course, no one can predict the future, but prioritizing and focusing finite research dollars in the right areas will be key to being positioned for success post-pandemic.

Will Cornish is a Vice-President at Explorer Research and works with a variety of CPG, Retailer, and other clients. He also heads up Explorer’s Media Testing Practice. He has 12 years of quantitative and qualitative research experience and before joining Explorer he was at TNS Canada.